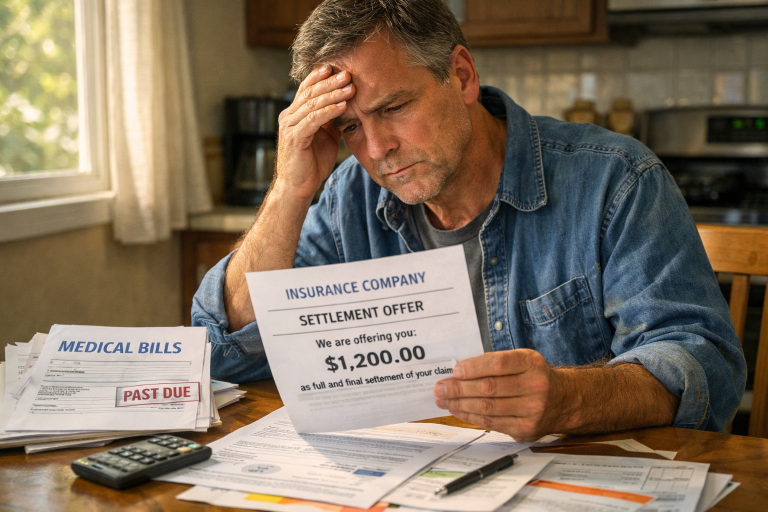

Following a car accident, many victims face mounting stress, medical bills, vehicle repairs, and lost wages. In the midst of this chaos, insurance adjusters often contact victims with a settlement offer soon after the incident. While accepting money quickly may seem like the easiest path, it is rarely in your best interest. Before making any decisions, it is wise to consult with a professional, such as a car accident attorney in Houston, to ensure your rights and financial well-being are protected. Insurance companies aim to resolve claims efficiently and for as little money as possible. Their initial offer may not fully account for the full spectrum of your damages, ongoing medical care, or future expenses. Settling too quickly can leave you facing financial hardship and limit your ability to recover true compensation for your losses.

Why Insurance Companies Make Lowball Offers

After an accident, insurance adjusters’ primary responsibility is to minimize the company’s payout. They often make a fast, low settlement offer, hoping you will accept before you understand the full costs. Most people are unfamiliar with the claims process or are overwhelmed by financial concerns and do not realize they can and should negotiate for more.

These first offers frequently ignore delayed symptoms, ongoing medical treatment, and long-term rehabilitation. Adjusters may also take advantage of the fact that victims are experiencing emotional distress and uncertainty, which can cloud judgment.

Insurance companies operate using sophisticated algorithms and databases that review thousands of similar accident claims, allowing them to build strategies that serve their best interests, not yours. Their objective is to close claims quickly, which helps them cut costs and maintain higher profit margins. Additionally, the initial offer may be “all-inclusive,” which may sound appealing but rarely covers vital elements such as future wage losses, additional hospital stays, or unanticipated therapy and medication costs. This is particularly risky in situations where injuries do not fully manifest until days or even weeks post-accident, making it even harder to estimate the final amount you may need.

Potential Risks of Accepting the First Offer

The biggest risk of accepting the first insurance settlement is waiving your right to any future compensation. Once you accept, you will likely be asked to sign a release. This legal document prohibits you from reopening your claim, even if you discover more severe injuries later. For example, symptoms like traumatic brain injuries, back problems, or even mental health challenges may not surface until days or weeks after the crash.

Furthermore, the money offered may not even cover immediate expenses, such as emergency room visits or vehicle replacement. Accepting without a full understanding of your expenses means you could be left paying out of pocket for damages that the at-fault party’s insurer should have covered. Another significant concern is that accepting a low offer makes it harder to negotiate a higher amount later, as insurers will cite your earlier acceptance as evidence that you considered their offer acceptable. This can impact your legal strategy and overall recovery. If unexpected complications or long-lasting effects develop over time, the funds you initially received may provide little relief, creating unnecessary financial and emotional strain for you and your family.

What Your Claim Is Really Worth

A fair settlement should account for both your short-term and long-term needs. Damages in car accident cases are typically divided into economic (medical bills, lost wages, property damage) and non-economic (pain and suffering, loss of enjoyment of life) categories. Calculating the full value of your claim often requires reviewing medical records, consulting outside experts, and projecting costs for continued care.

Many reputable resources stress the importance of evaluating all damages before entering settlement discussions. No two accidents or injuries are exactly alike, so a personalized assessment is crucial. Additionally, future losses, such as reduced earning capacity if you cannot return to your prior job, or the ongoing need for pain management and physical therapy, must be factored in. Loss of consortium, diminished ability to enjoy hobbies, transportation costs to and from medical appointments, and the potential for permanent disability are also relevant when determining the value of your claim. By resisting a quick settlement, you give yourself the best opportunity to account for these often overlooked or underestimated losses.

How to Respond to an Insurance Offer

When you receive the first settlement offer, remain calm and avoid agreeing to anything immediately. Carefully review the offer letter and compare it with your expenses and projected costs. It is wise to document all current and expected losses and consult legal and medical professionals. A strong counteroffer should be supported by documentation, including medical records, estimates of future treatment costs, and statements from doctors or accident reconstruction experts.

If you feel overwhelmed, advisors recommend seeking support from a professional, particularly for more serious claims. For more information on negotiating with insurance companies and understanding your rights, consider reviewing guidance from Consumer Reports.

Do not hesitate to seek clarification from the insurance company regarding how they calculated the amount in their offer. Request a comprehensive written explanation that details all categories of compensation included, and question any items that seem unclear or missing. Keep comprehensive records of all communications so you have a record if any disputes arise. In many cases, insurance companies anticipate some negotiation, so providing a well-supported counteroffer can result in a much higher settlement. Being persistent, polite, and organized can significantly influence the company’s willingness to negotiate further.

When Should You Settle?

You should only consider settling your car accident claim once you understand the full extent of your injuries, out-of-pocket costs, and long-term prognosis. This means waiting until your medical providers have a clear treatment plan and prognosis. If you are still undergoing treatment, it is often too early to accept a lump sum. With legal counsel, you can better evaluate whether the insurer’s offer is truly fair.

One way to determine if you are ready to settle is to ensure you have reached “maximum medical improvement” (MMI). This means your doctors expect no substantial improvement in your condition. Settling too soon can lead to significant regret if additional complications arise that require further care not reflected in your settlement. Conversely, dragging out the process unnecessarily can cause additional stress, so it’s important to strike a careful balance and rely on expert guidance.

Conclusion

Do not rush to accept the first insurance settlement after a car accident, as early offers are often lower than what you may be entitled to and may not cover future expenses. Carefully document all injuries, medical treatments, vehicle repairs, and other losses. Seek guidance from qualified professionals, including car accident attorneys and medical experts, before making decisions. Avoid signing any release without fully understanding your claim’s value. Educate yourself about your rights, remain patient, and resist pressure tactics. Proper documentation and professional advice are essential to maximizing your compensation and protecting your financial and legal future.